[ad_1]

For the reason that Nice Monetary Disaster in 2008-09, the revenue portion of portfolios has been virtually an afterthought. Your checking and financial savings accounts earned lower than 30bps; so too did the money sitting in your brokerage account. Equities did effectively, averaging ~14% throughout the 2010s, however Bonds, not a lot.

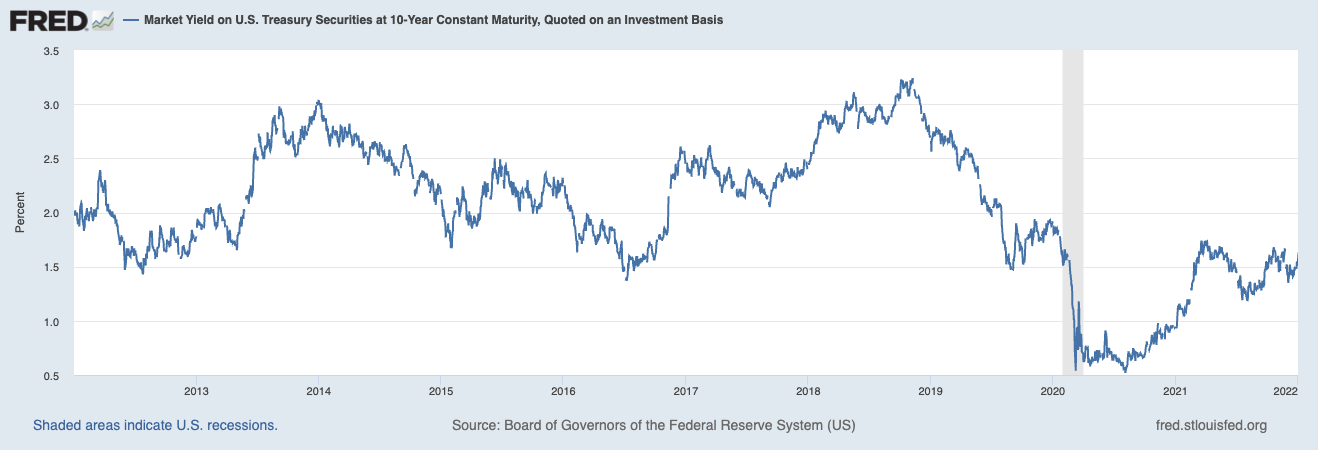

For the decade1 from 2012 to 2022, 10-year Treasuries yielded lower than 3% and averaged nearer to 2%. Funding grade Corporates gave you a little bit extra, between ~3-4% at considerably larger threat ranges with minimal default charges. Muni bonds have been yielding 2-3%, a tax equal (relying on the state you lived in and your tax bracket) of ~4-5%. And this was earlier than the 2022-23 charge mountain climbing cycle. That rate-hiking cycle all however ensures the following decade of fairness returns will look nothing just like the final decade.

However what the right-hand of upper charges taketh away from equities, the left-hand giveth to fastened revenue.

Because the fairness portion of your portfolio moderates (I recommend you decrease your return expectations for equities2 to ~5-7%), a lot of these lowered returns are being made up in fastened revenue.

After all, it is best to by no means let concern and greed drive your portfolio selections. What number of occasions have we mentioned individuals rising inventory market publicity late in a bull market or promoting shares as a bear market bottoms? However making modifications in fastened revenue is a matter of easy arithmetic — are you getting paid a enough yield relative to how lengthy you should tie up that capital? That is what governs the bond market. These are the forms of conversations we’ve been having with shoppers this 12 months at Ritholtz Wealth Administration.

Our funding committee made modifications in our fixed-income portfolios to benefit from larger charges; our advisors have been having conversations with shoppers about far more enticing choices they now have in fixed-income immediately versus final decade (sure, we wish to assume in many years in relation to fastened investing).

You probably have not been desirous about money administration and the yield alternatives the brand new charge regime has introduced, it’s not too late!

Within the first week of November, we’re bringing a giant crew to our places of work in North Carolina. We’re going to be assembly shoppers, advisors, and different people we don’t get to see in particular person all that usually. We will probably be internet hosting a dwell occasion on the Nascar Corridor of Fame (I’ll be doing just a few scorching laps), and broadcasting a dwell Compound and Associates from Charlotte to boost cash for “No Child Hungry.”

Along with equities, we will probably be discussing all the things from bespoke municipal bond portfolios to the best way to assemble a fixed-income holdings.

Considering chatting with us? We will probably be on the town November Fifth-Eighth. There are just a few slots left on the calendar; Ship an e-mail to information@ritholtzwealth.com with the topic line “Charlotte”

See you within the Tarheel State!

See additionally:Michael Batnick: If You’re On the lookout for a Change (October 23, 2023)

Josh Brown: There are 4 million households in North Carolina (October 24, 2023)

Me: RWM is Coming to Charlotte! October 11, 2023

Beforehand:Understanding Investing Regime Change (October 25, 2023)

{Dollars} Are For Spending & Investing, Not Saving (October 20, 2023)

Farewell, TINA (September 28, 2022)

__________

1. I purposefully selected the ten years previous to the FOMC 500 BPS rate-raising regime.

2. As mentioned earlier this week, there was a regime change within the dominant type of authorities stimulus, shifting from Financial to Fiscal.

The important thing takeaways have been this fiscal spending will stimulate the economic system, however larger rates of interest will finally stress family spending and company earnings, and that’s the reason it is best to decrease your return expectations for equities.

[ad_2]

Source link